学习笔记:可模拟(小市值+便宜 的修改版)

来源:https://uqer.io/community/share/566e867d228e5b7b41cfaf01

#小市值,低股价可模拟策略

import numpy as np

from heapq import nlargest, nsmallest

from CAL.PyCAL import *

import operator

start = '2015-01-01'

end = '2015-11-25'

benchmark = 'HS300' # 策略参考标准

#以沪深300、中证500、创业板的并集为股票池(中间存在一定交叉,因此需要去掉重复项)

universe = list(set(set_universe('HS300')+set_universe('ZZ500')+set_universe('CYB')))

capital_base = 10000

stk_num = 10 # 持仓股票数量

refresh_rate = 1

def initialize(account):

pass

def handle_data(account):

cal = Calendar('China.SSE')

# ----------------- 清洗universe --------------------------------

date = account.current_date #类型为datetime Date.fromDateTime(datetime) 将datetime转为Date,反过来 Date.toDateTime()将Date转为datetime

yesterday = cal.advanceDate(date, '-1B', BizDayConvention.Following)

yesterday = datetime(yesterday.year(), yesterday.month(), yesterday.dayOfMonth()).strftime('%Y%m%d')

fivedays = cal.advanceDate(date, '-5B', BizDayConvention.Following)

fivedays = datetime(fivedays.year(), fivedays.month(), fivedays.dayOfMonth()).strftime('%Y%m%d')

# 选出可用的300只市值最小的股票(如过用 universe = StockScreener(Factor('LCAP').nsmall(300))则不能进行模拟)

# MktStockFactorsOneDayGet函数支持的股票池长度有限,所以分两次合成Dataframe

LCAP = DataAPI.MktStockFactorsOneDayGet(tradeDate=yesterday,secID=account.universe[0:len(account.universe)/2],field=['LCAP','secID'])

LCAP = LCAP.append(DataAPI.MktStockFactorsOneDayGet(tradeDate=yesterday,secID=account.universe[len(account.universe)/2:],field=['LCAP','secID']))

LCAP = LCAP.sort_index(by = 'LCAP')

#这里我们将股票池转移到自己定义的my_universe中,不能修改account.universe,因为一旦修改则会导致模拟无法正常进行

my_universe =[i for i in LCAP['secID']][0:300]

# 去除ST股

try:

STlist = DataAPI.SecSTGet(secID=my_universe, beginDate=yesterday, endDate=yesterday, field=['secID']).tolist()

my_universe = [s for s in my_universe if s not in STlist]

except:

pass

# 去除流动性差的股票

tv = account.get_attribute_history('turnoverValue', 20)

mtv = {sec: sum(tvs)/20. for sec,tvs in tv.items()}

my_universe = [s for s in my_universe if mtv.get(s, 0) >= 10000000]

# 去除新上市或复牌的股票

opn = account.get_attribute_history('openPrice', 1)

my_universe = [s for s in my_universe if not (np.isnan(opn.get(s, 0)[0]) or opn.get(s, 0)[0] == 0)]

# 去除弱势股票

hist_prices = account.get_attribute_history('closePrice', 5)

hist_returns = {sec: hist_prices[sec][-1]/hist_prices[sec][0] for sec in hist_prices.keys()}

my_universe = [s for s in my_universe if hist_returns.get(s, 0) > 0.96]

#选出价格最小的stk_num*2只股票

bucket = {}

for stk in my_universe:

bucket[stk] = account.referencePrice[stk]

'''这里我们其实取了股价最低的 stk_num*2 只,原因在于:如果取stk_num只,

那么一旦遇到涨停停牌等买不进的情况,就跪了;所以我们拿stk_num*2 数量的股票,

但是却将仓位分成stk_num份,买进可以交易的前stk_num只股票'''

buy_list = nsmallest(stk_num*2, bucket, key=bucket.get)

# ----------------- 调仓逻辑 --------------------------------

clo = account.get_attribute_history('closePrice', 5)

target_increase1 = sum(clo[stk][-1] for stk in buy_list)/sum(clo[stk][-2] for stk in buy_list)

target_increase2 = sum(clo[stk][-2] for stk in buy_list)/sum(clo[stk][-3] for stk in buy_list)

target_increase5 = sum(clo[stk][-1] for stk in buy_list)/sum(clo[stk][0] for stk in buy_list)

dapan = DataAPI.MktIdxdGet(ticker=u"000300",beginDate=fivedays,endDate=yesterday,field=['closeIndex'],pandas="1")

dapan_increase = dapan['closeIndex'][4] / dapan['closeIndex'][0]

#止损逻辑,主要根据:最近两天的合计涨跌幅、上一天与五天前的合计涨跌幅、大盘的5天涨跌幅来作为限制条件

#满足条件则买入股票

if dapan_increase >= 0.963 and target_increase1 >= 0.963 and target_increase2 >= 0.963 and target_increase5 >= 0.963:

# 目前持仓中不在buy_list中的股票,清仓

for stk in account.valid_secpos:

if stk not in buy_list:

order_to(stk, 0)

money = account.referencePortfolioValue / stk_num

for stk in buy_list:

#不够一手最少买一手

order_to(stk, max(int(money / account.referencePrice[stk] / 100),1) * 100)

#不满止损条件则清仓

else:

for stk in account.valid_secpos:

order_to(stk,0)

return

本文主要是为了分享学习心得,希望能对和我一样的新人有所帮助。 写本文的动机主要是: 一、自己也是近期在优矿上开始模拟研究策略,觉得优矿提供的接口非常全面,并且注释详尽,让我这个新手对如何用python编写策略很快有了一个直观的认识(当然并不深入,但这已经非常好了),在量化这个本身就比较高门槛的领域,优矿能让新人有这种感觉和体验是十分难得和至关重要的,尤其在学习过程中,这是必不可少的一部分。 二、“为策略写代码注释是一个不错的学习方式”,这是一位朋友和我推荐的方法,这里也用自己的亲身体验和大家分享一下这个方法(大神请忽略我哈),确实对刚开是学习有很大帮助。

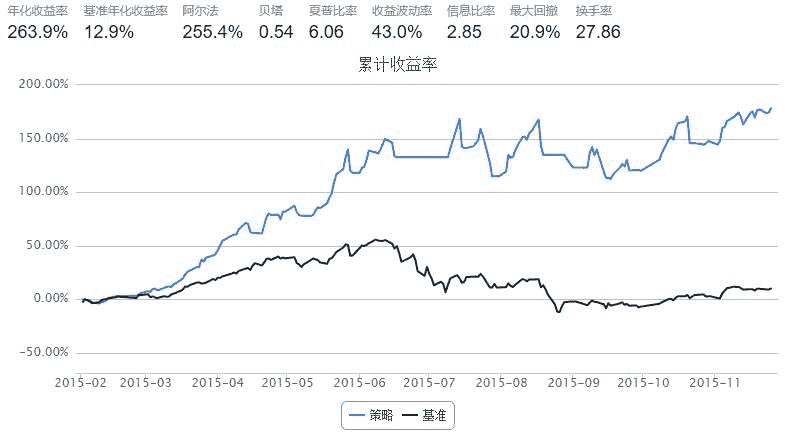

社区中有一篇“小市值+便宜就是Alpha”的策略,但是因为接口的原因不能模拟,刚好就以此为例:自己在给策略添加注释的同时,也将这个策略进行了一下修改,最终可以实现模拟运行,并可以考虑根据每天的交易信号实盘跟单。

本人是新人菜鸟,不足之处请大家多多见谅,多多批评指正,谢谢。