11.1 VWAP · Value-Weighted Average Price (VWAP)

来源:https://uqer.io/community/share/55462234f9f06c1c3d688033

You can find it in API doc

start = '2011-01-01' # 回测起始时间

end = '2015-01-01' # 回测结束时间

benchmark = 'SH50' # 策略参考标准

universe = set_universe('SH50')

capital_base = 100000 # 起始资金

longest_history = 40 # handle_data 函数中可以使用的历史数据最长窗口长度

refresh_rate = 1 # 调仓频率,即每 refresh_rate 个交易日执行一次 handle_data() 函数

threshold = 0.03

def initialize(account): # 初始化虚拟账户状态

pass

def handle_data(account): # 每个交易日的买入卖出指令

for s in account.universe:

try:

inter = 20

hist = account.get_symbol_history(s, inter)

except:

continue

vwampvalue = sum(hist['turnoverValue'])/sum(hist['turnoverVol'])

if(hist['lowPrice'][-1] < vwampvalue*(1 - threshold)) and (s not in account.valid_secpos):

order(s,100)

if(hist['lowPrice'][-1] > vwampvalue) and (s in account.valid_secpos):

order_to(s,0)

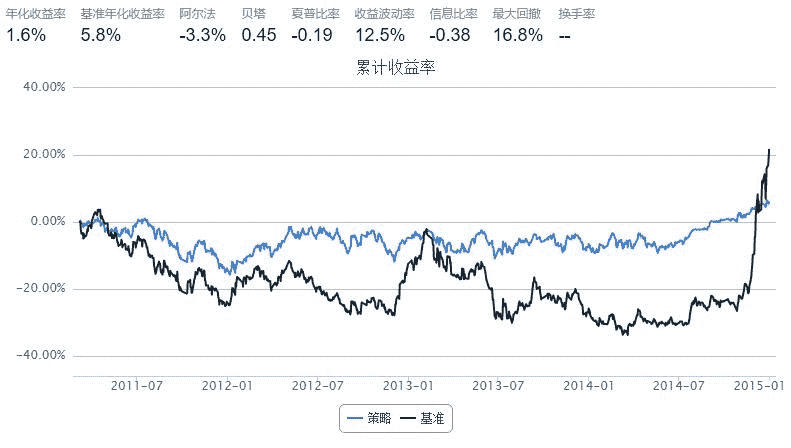

easy strategy.. bad results....

It's very difficult to get a good alpha......