macross

来源:https://uqer.io/community/share/55a92cdcf9f06c57a11b53be

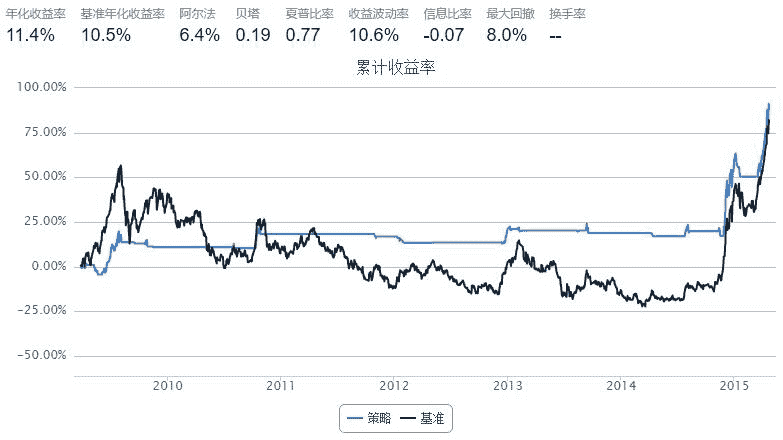

#第一次写大家帮看看有问题么

#策略 : 日收盘价高于ma20 买入; 低于ma20 卖出清仓

from matplotlib import pylab

import numpy as np

import pandas as pd

import DataAPI

import seaborn as sns

sns.set_style('white')

################

start = datetime(2008, 1, 1) # 回测起始时间

end = datetime(2015, 4, 23) # 回测结束时间

benchmark = 'SH50' # 策略参考标准

universe = ['510050.XSHG'] # 股票池

#benchmark = 'HS300'

#universe = ['510300.XSHG']

capital_base = 100000 # 起始资金

commission = Commission(0.0,0.0)

window_short = 20

window_long = 300

longest_history = window_long

#longest_history = window_short

SD = 0.05

def initialize(account): # 初始化虚拟账户状态

account.fund = universe[0]

account.SD = SD

account.window_short = window_short

account.window_long = window_long

def handle_data(account): # 每个交易日的买入卖出指令

hist = account.get_history(longest_history)

fund = account.fund

short_mean = np.mean(hist[fund]['closePrice'][-account.window_short:]) # 计算短均线值

long_mean = np.mean(hist[fund]['closePrice'][-account.window_long:]) #计算长均线值

now_price = hist[fund]['closePrice'][-1:]

#print len(short_mean)

#print type(now_price)

#print(now_price)

#now_price.plot

#all_close_prices = account.get_attribute_history('closePrice', 1)

# 计算买入卖出信号

# flag = True if (short_mean - long_mean) > account.SD * long_mean else False

flag = True if (now_price - short_mean) > account.SD * short_mean else False

if flag:

if account.position.secpos.get(fund, 0) == 0:

# 空仓时全仓买入,买入股数为100的整数倍

approximationAmount = int(account.cash / hist[fund]['closePrice'][-1]/100.0) * 100

order(fund, approximationAmount)

else:

# 卖出时,全仓清空

if account.position.secpos.get(fund, 0) >= 0:

order_to(fund, 0)