便宜就是 alpha

来源:https://uqer.io/community/share/5609169cf9f06c597565ef13

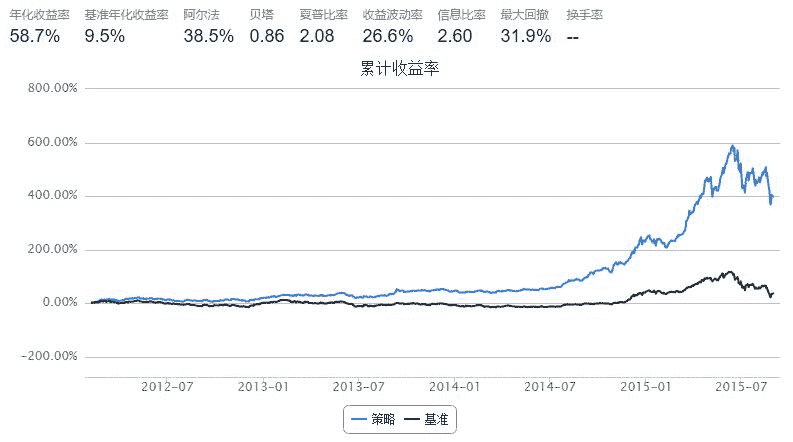

参考社区的策略,练手一个简单的调仓逻辑

策略思路

- 一星期或者一个月一换仓

- 每次换仓时,取股价最低的15只等权重买入

import numpy as np

from heapq import nlargest, nsmallest

from CAL.PyCAL import *

start = datetime(2012, 1, 1)

end = datetime(2015, 8, 31)

benchmark = 'HS300' # 策略参考标准

universe = set_universe('ZZ500') + set_universe('HS300')

capital_base = 1000000

stk_num = 15 # 持仓股票数量

refresh_rate = 5

def initialize(account):

pass

def handle_data(account):

cal = Calendar('China.SSE')

# ----------------- 清洗universe --------------------------------

date = account.current_date

yesterday = cal.advanceDate(date, '-1B', BizDayConvention.Following)

yesterday = datetime(yesterday.year(), yesterday.month(), yesterday.dayOfMonth()).strftime('%Y%m%d'),

# 去除ST股

try:

STlist = DataAPI.SecSTGet(secID=account.universe, beginDate=yesterday, endDate=yesterday, field=['secID']).tolist()

account.universe = [s for s in account.universe if s not in STlist]

except:

pass

# 去除流动性差的股票

tv = account.get_attribute_history('turnoverValue', 20)

mtv = {sec: sum(tvs)/20. for sec,tvs in tv.items()}

account.universe = [s for s in account.universe if mtv.get(s, 0) >= 10**7]

# 去除新上市或复牌的股票

opn = account.get_attribute_history('openPrice', 1)

account.universe = [s for s in account.universe if not (np.isnan(opn.get(s, 0)[0]) or opn.get(s, 0)[0] == 0)]

# ----------------- 调仓逻辑 --------------------------------

bucket = {}

for stk in account.universe:

bucket[stk] = account.referencePrice[stk]

# 以前面计算得到的turnover_delta对股票池中股票排序,并取前stk_num只,力图满足比赛要求

# 注意:

# 这里我们其实取了股价最低的 stk_num*2 只,原因在于:为了满足参赛要求,调仓时候我们必须

# 达到一定仓位,如果取stk_num只,那么一旦遇到涨停停牌等买不进的情况,就跪了;所以我们拿

# stk_num*2 数量的股票,但是却将仓位分成stk_num份,每份买进一只,这样有一只买不进,就

# 买后面的,参赛调仓是不是保险了许多啊

buy_list = nsmallest(stk_num*2, bucket, key=bucket.get)

# 目前持仓中不在buy_list中的股票,清仓

for stk, amount in account.valid_secpos.items():

if stk not in buy_list:

order_to(stk, 0)

# buy_list中的股票,等权重买入

position_per_stk = account.referencePortfolioValue/stk_num # 将仓位分成stk_num份

for stk in buy_list:

if account.referencePrice[stk] > 0:

amount = int(position_per_stk/account.referencePrice[stk]/100.0) * 100

order_to(stk, amount)

return